Income Contingent Repayment (ICR)

Income Contingent Repayment (ICR) is the original income-driven repayment plan for federal student loans, first eligible in 1994. ICR is available only to those borrowers with federal Direct Loans.

ICR is the only income-driven plan available to Parent PLUS borrowers if the parent loans are consolidated into a Direct Consolidation Loan.

Calculated payments under ICR are the lesser of

- 20% of your discretionary income; or

- The amount you would pay under a fixed 12-year repayment plan, adjusted by a factor based on your adjusted gross income (AGI).

It is possible for ICR payments to be less than the interest which accrues each month (negative amortization). Any unpaid interest is added to your principal (capitalized) each year when new income documentation is due. There is a cap on the amount of unpaid interest that can be capitalized, equal to 10% of your starting repayment balance. Once that cap is reached, further unpaid interest accrues, but does not capitalize.

ICR payments are made for a maximum repayment period of 25 years. Any principal and interest that remains after 25 years of qualifying payments will be forgiven.

Why you should care about ICR

Very few borrowers use ICR. Unfortunately, the complicated monthly payment calculation routinely results in a higher monthly payment compared to any other income-driven repayment plan. While it is often lower than a fixed 10-year plan payment, there is nearly always a repayment plan that will result in a more beneficial payment than ICR.

However, with the recently announced one-time forgiveness count adjustment, ICR can be a beneficial repayment plan for borrowers who still have limited forgiveness-qualifying repayment time remaining before receiving forgiveness after the count adjustment is applied. Refer to the blog on consolidating your loans to benefit from the one-time count adjustment for more detailed information on this special case for ICR.

Calculating your ICR monthly payment:

ICR has the most complicated monthly payment calculation. The resulting monthly payment is the lesser of two calculations.

Step 1) The easier of the calculations is 20% of your discretionary income:

ICR Discretionary Income A = Your AGI - HHS federal poverty guidelines

(A note that the ICR formula is different from IBR, PAYE, and REPAYE formulas)

20% * ICR Discretionary income divided by 12 = payment per month

Step 1 Example: Let’s say you're calculating your 2025 ICR Discretionary Income for a family size of 3 with a most recent 2023 AGI of $130,000. Your remaining student loan balance is $100,000 at 6%.

ICR Discretionary Income = $130,000 - $26,650 = $103,350

Your monthly ICR payment might be 20% of your Discretionary Income divided by 12:

example ICR payment = 0.20*$103,350 = $20,670 annually or $1,723 per month

Step 2) The more complicated of the calculations has two parts:

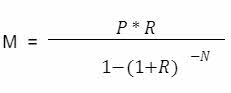

2a) Fixed 12-year monthly payment:

M = monthly payment;

P = principal balance when entering repayment;

R = Monthly Interest Rate;

N =Number of monthly payments

Step 2 Example: Your student loan balance is $100,000 at 6%.

2b) The income factor multiplied by the fixed 12-year monthly payment

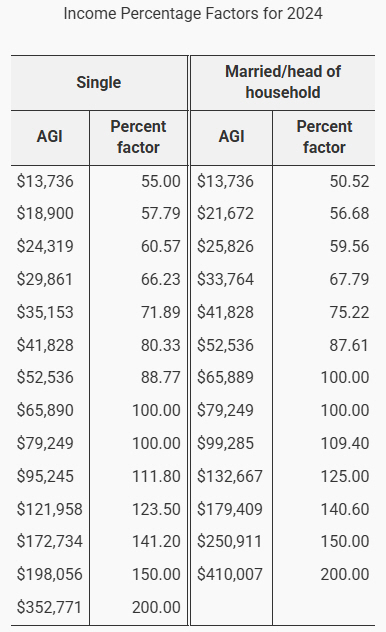

Source: Annual updates to ICR plan formula 2024

Essentially, if your taxable income is between $65,890 and $79,249 for a single or married household, respectively, then your ICR calculation will equal the fixed 12-year plan payment. Below that range your ICR calculation will be less than the fixed 12-year plan payment. Above that range your ICR calculation will be more than the fixed 12-year plan payment.

Let’s return to our previous example of a family size of 3 with a taxable income of $120,000. According to the table, the factor we need is between 109.4 and 125 and will be closer to 125 than 109.4. We do a linear interpolation to arrive at the exact factor:

(Table, AGI) $124,811 - $93,405 = $31,406 (a)

(Table, % Factor) 125% - 109.4% = 15.6% (b)

$120,000 (borrower AGI) - $93,405 (Table, AGI) = $26,595 (c)

$26,595 (c) / $31,406 (a) = 84.7% (d)

15.6% (b) * 84.7% (d) = 13.2% (e)

109.4% (Table, % Factor) + 13.2% (e) = 122.6% (f)

$976/mo (12-year plan amount) * 1.23 (f) = $1,200/mo

In this example, the fixed 12-year monthly payment adjusted for income calculated in step 2 is less than the discretionary income calculation in step 1; thus the ICR minimum monthly payment would be $1,200/mo for the next 12 months.

You must provide yearly documentation of your income in order to have a payment calculated using an ICR formula. If you fail to provide timely documentation, your payment will revert to the standard 10-year repayment amount when the loan entered ICR, and any unpaid interest will be capitalized until the unpaid interest capitalization cap is reached (10% of your starting repayment balance). Provide timely and appropriate income documentation to remain in any income-driven repayment plan and limit unpaid interest capitalization.